Whiteout Capital

Private investor publishing independent research focused on microcaps.

Kraken Robotics (TSXV: PNG)

Published: May 25, 2023

*Note that financials are stated in CAD

Summary

Kraken Robotics (TSX: PNG $117.5MM CAD) is a subsea intelligence company serving defense and commercial customers. Their business can roughly be broken into four main segments/products:

- AquaPix: their synthetic aperture sonar (SAS) sensor that can be purchased as a standalone product and installed on various types of underwater vehicles and vessels.

- Katfish: unmanned-underwater vehicle (UUV) equipped with AquaPix that is towed behind a boat to collect high-resolution acoustic images of the seafloor.

- SeaPower: pressure-tolerant deep sea batteries for autonomous underwater vehicles (AUVs)

- Robotics-as-a-service (RaaS) via PanGeo: service-based business segment that offers seafloor mapping, sub-seabed mapping, and 3-D laser imaging.

On May 1st, the company posted an update with 2023 FY guidance of $66-78MM revenue and $12-17MM EBITDA with $5-6MM capex. At the midpoint of $72MM revenue and $14.5MM EBITDA, the company would grow 76% YoY, and EBITDA would expand by 275%. At $5.5MM capex, this would also generate $9MM of FCF.

Furthermore, I believe their revenue forward guidance is nearly entirely guaranteed based on contracts announced within the last year that will payout in 2023 (I expand on this below). If anything, they have the potential to far exceed these estimates if they were to land more large contracts.

With an enterprise value of $124.5MM, this implies the company is trading at 1.7x revenue, 8.6x EBITDA, and 13.8x FCF based on forward 2023 numbers. I believe these multiples are low given the high barriers that exist in their industry, the fact that they’ve sustained gross margins in the low to mid-40s for many years and that they’ve grown reported revenue from 3.5MM in 2017 to $40.9MM in 2022, >50% annualized.

Despite these positive developments, the share price is essentially flat over the last five years. There are three main factors that have held the share price back:

First, the founder and past CEO, Karl Kenny, is a brilliant innovator and entrepreneur, but he has made a habit of raising money and/or selling stock every time the share price jumps on good news. On December 22, 2022, the company announced that Karl would be stepping down as CEO and moving into an Executive Chairman position and that longtime CFO Greg Reid would take over as CEO. Greg has been deeply involved in the business for many years and early indications show that he’s more focused on delivering shareholder value and improving margins.

Karl currently owns 19.56MM shares (~9.7% of the company) and continues to sell large volumes of shares at critical times. His ownership is down from 27.7MM shares a few years ago, which was also before significant dilution occurred.

Greg owns 7.86MM shares (~3.9%) and has been a consistent buyer on the open market, including a private purchase of 3MM shares direct from Karl on August 19, 2022. In fact, of the seven insiders who’ve made stock transactions in the last year, Karl is the only one who has sold, with most insiders adding meaningfully to their position.

I haven’t been able to get a clear answer on what Karl’s endgame selling plan is (i.e. does he want to get down to X%). I like that Greg purchased a large block of shares from him directly, but if he wants to decrease his stake meaningfully from current levels, it’d be nice if he could go out and find a buyer rather than dump shares onto the open market every time the price starts to run. The company more than doubled its share count in the last six years, so I’m not sure why he chose to sell on the open market rather than sell shares in one of the offerings. Even as recently as the week of May 13th, Karl sold 500k shares on the tail of a $16MM battery contract announcement, which led to no movement in the share price. He should have less of an impact on share price going forward, though his selling habits continue to be a shorter-term risk.

Second, the company has never been profitable and has relied on raising a substantial amount of capital over the past decade. I believe Kraken is finally on the brink of profitability. The company generated $100k of FCF last year with only $200k of stock issued, so they are already near breakeven on a backward-looking basis, and that was with an EBITDA margin of just 7.4%. Guidance for FY 2023 implies a ~20% EBITDA margin and Greg recently stated that he thinks he can get the company to >30% EBITDA margins. With capex stabilizing in the $5-6MM/yr range in 2021, 2022, and guided 2023, these margins should support healthy FCF and earnings in the years to come.

The share count went from 91MM in 2017 to 201MM in 2021, but was essentially flat in 2022. Past raises were done in part to fund the delivery of large orders, but Kraken now requires a 25% upfront payment that will help cover the cost to build products prior to delivery. I also think that the lack of share issuance in 2022, combined with the company hopefully transitioning to profitability in 2023, is a positive sign that there won’t be significant dilution going forward. Given the company’s history, I don’t think anyone can say for certain that they won’t continue to issue shares, but I do think the odds are high.

Finally, the company’s revenue is based on signing large, non-recurring contracts, which makes revenue lumpy and unpredictable. While this is an aspect of the business that will never change, Kraken has significantly diversified its product and service offerings in the last few years, which should help smooth out revenue and provide diversification should one of the industries they operate in meet stiff headwinds.

I believe that by the end of 2023/2024 Kraken’s share price should increase substantially as their guided numbers and signed contracts are officially reported and that they are an attractive acquisition target. I’ll expand on both of these points in the sections below.

Business Operations

Sensors (2021-present)

Kraken’s first product was a synthetic aperture sonar (SAS) sensor called AquaPix, which offers customers a big upgrade on traditional side scan sonar.

The way that side scan sonar works is that a sensor sends an acoustic pulse towards the seafloor, waits for the waves to bounce off the bottom and return, reads in the data, and then repeats the process. The problem with this method is that the acoustic waves form a funnel shape, with the cone widening as they travel deeper, which results in lower-resolution imaging the deeper you scan.

SAS is a newer technology that sends out continuous acoustic pulses and reads the combined data as the signals return to paint a more complete picture. The result is an improvement of up to 30x the resolution of side scan at any given depth.

The difference in detail between an image collected with SAS and one with side scan is pretty remarkable. To see a side-by-side comparison, go to minute 9:00 of this video.

The one drawback of SAS is that it needs to be attached to an unmanned underwater vehicle (UUV) and towed at a constant speed and in a straight line. Side scan would no doubt also be negatively affected by intentionally chaotic boat driving, but since SAS sends out a continuous beam of sound, the speed needs to be constant or the readings won’t turn out.

SAS is not simple to execute and there are only three companies in the world with a competing product—Northrop Gruman, Thales, and Kongsberg. Comparing these SAS sensors to one another, Kraken is the best or tied for the best by every measure, producing high-resolution images, operating in the deep ocean, and covering a large area with each pass.

Kraken also makes industry-leading 3-D laser scanners, which are sold under the name SeaVision. Unlike AquaPix, these sensors are typically installed on autonomous UUVs (AUVs) that can journey to the seabed, close to what needs to be scanned. These laser scanners, in conjunction with Kraken’s software, can 3-D map chains, pipes, and other infrastructure on the sea floor, then layer on color-coded analytics to the rendering to visualize essential properties, such as corrosion. Common customers include oil & gas and offshore wind companies.

SeaPower (2017-present)

As Kraken’s sensors were sold and installed on UUVs made by other companies, they started designing components that enabled them to further increase the quality of their sonar scans. Two main products came out of this R&D, their SeaPower batteries and their rim-driven thrusters.

The rim-driven thrusters help stabilize a UUV as it’s moving through the water, which reduces noise on the sonar scans. They originally acquired their battery tech through a $1MM acquisition of a German company.

Kraken’s new CEO, Greg, has mentioned several times in company presentations that near outer space is better explored and understood than the depths of our oceans. Deep ocean environments are harsh and difficult to operate in as they subject equipment to a combination of high pressure, salt, and water that quickly corrodes and damages most man-made equipment.

Kraken’s designed their SeaPower batteries to perform in these difficult conditions. While older deep sea battery tech relies on thick metal pressure housings, SeaPower batteries use a novel silicon gel encapsulation that improves performance and decreases weight. On average, when UUVs replace their legacy batteries with a SeaPower battery of the same size, they operate for ~50% longer, are about 1/10th the cost, and can descend to depths of up to 6,000m.

While Kraken’s SAS sensors are best-in-class and can drive significant future growth, I believe their SeaPower batteries are the most valuable asset. One of Kraken’s largest recent customers has been Dive Technologies, which is owned by Anduril. For those unfamiliar with Anduril, they are a rapidly growing defense contractor founded by Palmer Luckey, who also founded and sold Ocular to Facebook. Anduril is on the cutting edge of defense technology and they equip their XLUUVs with Krakens SeaPower batteries and AquaPix sensors.

XLUUVs are large unmanned underwater vehicles that can do multi-day missions to collect data, disable mines, and perhaps even engage in anti-submarine warfare. They are not a competitor to Katfish as they serve totally different purposes.

In just the last six months, Kraken has received $30m worth of battery orders from an undisclosed customer, with the most recent contract valued at $16m for two batteries. While it’s not certain Anduril is the customer, I believe it is highly likely for two reasons. First, back in 2021 before Aduril acquired Dive Technologies, Kraken announced a SeaPower/AquaPix contract and testing with them explicitly named as the customer (here and here. They also stated that “The Dive-LD is also powered by Kraken’s pressure tolerant batteries.” Second, Greg has stated on more recent calls that Anduril continues to be a close and key partner.

Not only could these battery orders become more frequent if Anduril is successful in selling their products, but there are XLUUVs being designed that are the size of a school bus and equipping those with a SeaPower battery would be an even larger transaction. Furthermore, Anduril is just one of many companies working on larger battery-powered ocean vehicles and Kraken recently signed a battery testing agreement with the US Navy. Northrop, Boeing, and General Dynamics are all designing their own XLUUVs.

Katfish & Thunderfish (2018-present) In the early days, Kraken partnered with larger defense contractors and equipped their units with sensors, batteries, and thrusters. In 2018, the company launched two of their own UUVs:

Katfish: a towed UUV to collect sonar data.

Thunderfish: an autonomous UUV that can travel to depths of 6,000m and collect 3-D scans, sub-seabed imaging, and video.

The Thunderfish is no longer sold as a standalone product and is instead used in their Robotics-as-a-Service (RaaS) line of business launched in 2021 (see below), so I’m going to focus on Katfish in this section.

Katfish is a product sold mainly to defense customers. Kraken also sells their Tentacle Winch that can autonomously deploy and retrieve a Katfish. These are towed UUVs, which means they don’t have a motor and need to be pulled by a ship. However, they do have Kraken’s stabilizers that increase the quality of sonar scans and the units can be completely unmanned. The Israeli Navy has outfitted unmanned, autonomous boats with Katfish so that they can be deployed to mine hunt without the potential loss of human life.

Not only are Katfish equipped with Kraken’s SAS sensors, they also come with industry-leading real-time processing software that allows users to view the sonar data as images live (post-processing usually requires a high-tech worker to convert the data to images post-collection) and actively zoom and navigate the map while placing markers with notes on areas of interest to revisit in more detail later. The data is saved locally for later investigation, but it can also be live-streamed directly to a computer in the cabin of the towing ship or even back to an on-shore base if there is a supporting satellite connection.

Katfish can collect 3cm resolution images at speeds of up to 10 knots at an area coverage rate of 4 km^2/hr. Like their SAS and battery tech, the Katfish is a best-in-class product in terms of quality and there are only a few competitors that can offer something close.

A few recent customers include the Canadian Royal Navy ($50MM contract announced December 7, 2022), Danish Navy ($36MM contract announced September 8, 2020), and Polish Navy (est. $10MM announced September 8, 2020).

Robotics-as-a-Service (2021-present) In 2021, Kraken acquired a Scottish company called PanGeo that specialized in sub-seabed imaging (underground). Over the years, Kraken found that while defense customers were willing to spend $5m on a Katfish, the functionality of their Thunderfish better fit commercial customers who needed to inspect assets on the sea floor, but didn’t want to own their own equipment. By combining their Thunderfish AUV and SAS technology with PanGeo’s sub-seabed expertise, the company launched its Robotics-as-a-Service (RaaS) line of business.

The RaaS business segment services a wide range of customers including oil & gas, offshore wind, subsea cables, and the emerging market of subsea mineral extraction. Their services often include a mix of high-resolution sonar imaging, 3-D mapping and predictive modeling of equipment on the seafloor, and sub-seabed analytics.

While the contract sizes for this line of business are generally smaller than Katfish and SeaPower, it gives them another way to utilize their technology and service customers outside the defense industry. Most of their competitors on high-end sonar and UUV projects are large defense contractors who won’t take the time to offer these types of surveys in the commercial space, so I believe their product offering is unique and potentially a very valuable asset.

Competitive Landscape

As stated earlier, Kraken is one of four companies globally that produces high-quality SAS sensors—Northrop, Thales, and Kongsberg being the other three. Kongsberg only sells their SAS sensors on their Hugin AUV and Thales primarily only sells their sensors on their own towfish. Northrop does sell SAS sensors, but they are significantly more expensive than Kraken’s and often because of Internation Traffic in Arms Regulations (ITAR), they don’t compete much outside of the US. As far as SAS sensors go that can be installed on a variety vehicles, Kraken offers the best specs at the lowest price and their main competitor can’t operate in most of the global market.

Their main competitors in the towfish market are Thales, Northrop, ECA Robotics, and Klein, as these are the only companies that offer both a towfish and high-quality sonar.

Klein only has side scan sonar and their products often don’t meet bid requirements. Kraken’s IR told me that, “even if they barely meet the specifications, we are seeing most all Navies now favoring SAS over SSS at time of award.”

ECA Robotics produces their Allister AUVs and does not have a SAS product that they currently sell. They have purchased SAS sensors from Kraken in the past to equip their UUVs, but are trying to develop their own. They won a contract with the Belgium Navy back in 2018 that Kraken competed on. From Kraken’s IR, “ECA won the Belgium program back in 2018. They still have not delivered on that program while we have delivered 4 KF System for the Danes, 1 system to Poland, and 1 system to Australia. In the end they won that program which included everything from UUVs to USVs to minehunter ships, as their consortium saw the shipbuilder cut a couple hundred million Euro off of the ship price. Could have cut the minehunting equipment price in half and still wouldn’t have won as the ship price moved the needle.” As per this contract, ECA is developing SAS to fulfill this order, but four years in and they haven’t made tangible progress.

That leaves Thales and Northrop, which I consider Kraken’s main competitors. Northrop sells their AQS-24B towfish equipped with SAS, but their units are typically around double the price of Kraken’s, and as mentioned above, they mainly service the US Navy and are often restricted from selling technology internationally.

Thales is probably their strongest international competitor and in the years ahead they will likely win a few contracts over Kraken. However, I think Kraken will continue to win a good proportion and they have already beaten Thales on large contract bids, including the 2020 Danish Navy contract.

There are many suppliers of just AUVs, including ECA, Teledyne, Kongsberg, Nauticus Robotics, Anduril, BAE, MSubs, Cellula, ISE, and IAI Elta. However, these suppliers often have to come to Kraken for SAS and batteries and recently NATO navies have been favoring a complete solution for their mine-hunting units.

As far as I can tell from my research, Kraken’s battery technology has no close competitors. Most subsea batteries are pressurized, which requires a thick metal casing and oil encapsulation. Kraken’s silicon gel encapsulation enables them to sell batteries at 1/10th the cost of traditional batteries and their batteries typically last ~50% longer for a battery of identical dimensions and weigh considerably less. Other companies are likely working on competing products, but for now, Kraken is the clear winner.

Finally, their RaaS business operates in a competitive industry, but I do still think this business segment has a lot of promise because of their unique positioning. Most competing surveying companies make the bulk of their money on the daily ship rate, which is typically $100-200k/day. None of Kraken’s sonar competitors operate in this industry as they are primarily defense contractors. These surveying companies have traditionally had to purchase tech from companies like Kraken and train people to run it.

Kraken now offers a full solution, and as far as I can tell, they are the only company with their own SAS, 3-D imaging, and subsea bed mapping technology that also offers a physical service. Furthermore, the surveying companies are mostly in the game for the large daily ship rates and early indications suggest that they are happy to throw Kraken a $5-10MM bone in order to rake in the $100-200k/day ship rate and avoid the cost of buying equipment and staffing people to run it.

Here is a list of all of Kraken’s competitors that I’ve been able to track down. I added quotes from conversations I’ve had with IR, who spoke with people at Kraken.

- Northrop (US)

- From IR, “Northrop generally play in the US and we don’t see them much outside the US as ITAR is often an issue and a lot of the non US navies are looking for reasonably priced solutions as opposed to Northrop which is very expensive.”

- Hunter (XLUUV non-competitor): https://www.militaryaerospace.com/unmanned/article/14207881/unmanned-underwater-vehicle-uuv-payload-delivery-sensors

- AQS-24B (Katfish competitor): https://www.northropgrumman.com/what-we-do/sea/aqs-24b-minehunting-system/

- From IR, “We beat them out in Denmark. They are strong with US Navy. Unlikely to have success in international market that much.”

- µSAS senso (AquaPix competitor): https://news.northropgrumman.com/news/releases/northrop-grumman-to-integrate-sonar-system-onto-l3harris-unmanned-undersea-vehicle

- From IR, “Competitor to our man portable SAS which we developed since 2019 under FCT program funding. We are getting traction with US and UK and international customers with our man portable SAS. Some of our recent PR which don’t name customers are for this product. Northrup microSAS is 2x the price of ours and we still make very good margins on ours. Tech similar”

- Thales (France):

- Strong competitor that offers UUVs with SAS sonar of similar quality. They compete best with Kraken on the combo of tech and price.

- Eca Robotics (France):

- ROV (Katfish competitor): https://www.ecagroup.com/en/solutions/seabed-survey-rov

- From IR, “ECA produce Allister AUVs. They have bought SAS from us in the past to go on these. They won the Belgium program in 2018 or 2019 as per above and are developing their own towfish and their own SAS. 4 years later we haven’t seen it yet but they likely will eventually get there.”

- ROV (Katfish competitor): https://www.ecagroup.com/en/solutions/seabed-survey-rov

- Klein (subsidiary of MIND Technology)

- Conventional sidescan and often aren’t even considered as they don’t meet the technical specs of most bid requirements. From IR, “even if they barely meet the specifications, we are seeing most all Navies now favoring SAS over SSS at time of award.”

- Kongsberg

- Hugin AUV—battery operated, not towed

- Has SAS, but only sells it pre-installed on Hugin

- Anduril (US)

- Dive-LD (XLUUV non-competitor): https://www.anduril.com/hardware/dive-ld/

- From IR, “Emerging player in the space. They bought Dive Technologies (Ex Bluefin / General Dynamics team that formed a startup). Dive was using our batteries and SAS and now Anduril is. So we in effect provide the ears and engines of their UUVs.”

- Lockheed Martin (US):

- Marlin AUV (Katfish competitor): https://www.lockheedmartin.com/en-us/products/marlin.html

- From IR, “Marlin is not a towfish, but a battery operated AUV. We have sold several SAS to Lockheed over the years for the Marlin AUVs.”

- AN/WLD-1 Sonar (AquaPix competitor): https://en.wikipedia.org/wiki/AN/WLD-1_Remote_Minehunting_System

- From IR, “Believe that program is end of life. Was a billion $ boondoggle that became the posterchild in the US Navy for inefficient spending.”

- Marlin AUV (Katfish competitor): https://www.lockheedmartin.com/en-us/products/marlin.html

- Atlas Elektronik (Germany):

- SeaCat (Katfish competitor): https://www.atlas-elektronik.com/solutions/mine-warfare-systems/seacat.html

- From IR, “Atlas have bought out SAS and use it on the SeaCat. They also bought a KATFISH from us a few years back. But they have for years been trying to develop their own SAS, so yes we view them as a competitor now,. They have not had much traction in the market on their AUVs.”

- HMS-12M Sonar (AquaPix competitor): https://www.atlas-elektronik.com/solutions/mine-warfare-systems/hms-12m.html

- From IR, “This is a Forward Looking, Hull Mounted Sonar which has been traditionally installed onboard MCM Vessels. This is not a competitor to SAS, since SAS is not mounted on Surface vessels, and this type of sonar is not capable of being mounted on AUVs and Towfish.”

- SeaCat (Katfish competitor): https://www.atlas-elektronik.com/solutions/mine-warfare-systems/seacat.html

- General Dynamic (US)

- Reliant & Black Pearl UUV (Katfish competitor): https://www.militaryaerospace.com/unmanned/article/14167361/uuv-satcom-sensor-payloads

- Also supply side-scan sonar systems

- From IR, “GD bought Bluefin in 2016 and that is how they got into the minehunting game. They have 1 main customer which is the US Navy for their Knifefish AUV. This is a very expensive solution that has been 10 years+ getting from concept to program of record.”

- Boeing (US)

- Orca (XLUUV non-competitor): https://www.militaryaerospace.com/unmanned/article/14207881/unmanned-underwater-vehicle-uuv-payload-delivery-sensors

- From IR, “Would compete against an Anduril who is our customer for SAS and batteries. XLUUV is an emerging market. They UUVs can do a variety of tasks such as ISR, minehunting, mine laying, etc. There are 6 or 7 companies coming with XL UUVS, Boeing will be US Navy’s choice to start, but again is extremely expensive. Unlikely to be a player in international markets due to cost and ITAR. We technically could sell SAS and batteries to them but we haven’t cracked that nut yet.”

Addressable Market

One of my early concerns with Kraken was that the addressable market was too small and that they’d hit a ceiling in the near future. I’m not a fan of using TAM estimations to value a business, so I want to be clear that this analysis is meant to demonstrate that they have not reached their TAM rather than to define an accurate TAM.

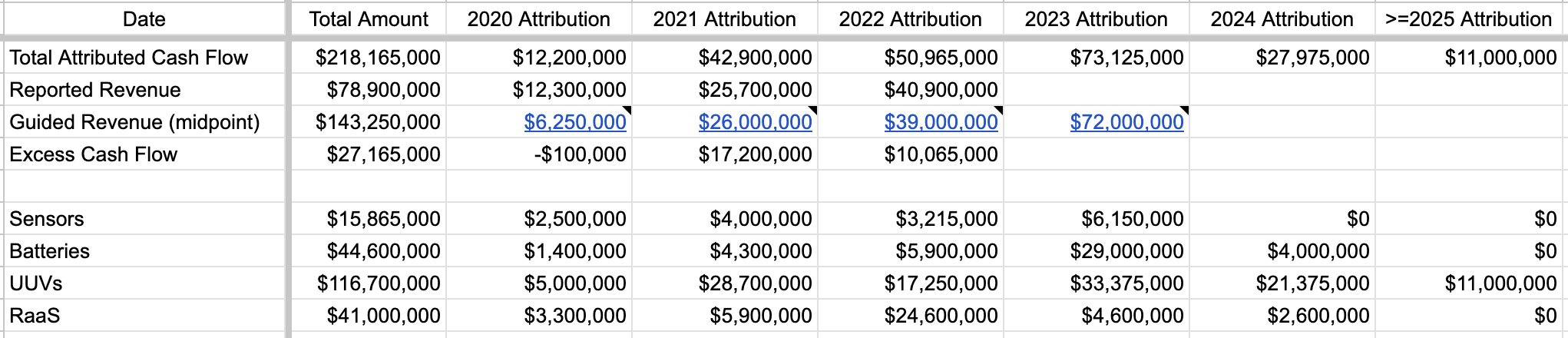

Here’s a table of reported contract values for each year, 2020 to present:

While the sensor business is having a good year, I think going forward it will play a minor role in overall revenue. The sensors typically sell for ~$500k each, so the larger Kraken gets, the more they will need to sell to move the needle. While Kraken’s sensors are versatile and can be fitted onto many vehicles, I don’t foresee revenue being able to sustain higher levels than $10-20MM/year.

In the medium term, I think they might need to raise the price of their sensors when sold as a standalone product. It’s made sense in the past to get paid $500k to outfit a competitor’s UUV on a missed contract, but going forward, it might be better to crowd out the other UUV players that don’t have SAS in order to push Katfish. The exception would be that perhaps sensors could also be sold with batteries or maybe there is a minimum order value of a few million dollars. Regardless of how they end up running the company, sensors alone will play a less important role going forward.

Greg stated recently that there are approximately 300 mine-hunting units globally that they could outfit. We are currently in the early stages of a large replacement cycle as >70% of them are at least 20 years old. As these units are upgraded, Kraken will likely win a fair number of contracts. My biggest concern here is that even if Kraken outfitted all 300 mine-hunting units with a Katfish, that’d total $5MM*300 = $900MM. If these vehicles have a twenty-year life, that averages out to just $45MM/year. Since the replacement of these units is not uniform, we are probably in a 5-10 year stretch where, say, 70% of the units will be replaced. So the opportunity for the foreseeable future is probably more like $100-150MM/year. If Kraken can take just a third of that, they still have a decent growth runway, but equipping mine-hunting ships likely isn’t going to be what takes them from $72MM to $500MM in annual revenue.

There is a high likelihood that the number of mine-hunting globally will expand, especially given rising geopolitical tensions. There are also emerging markets for unmanned surface vessels with towed SAS (as described above in the Israeli Navy). The unmanned surface vessels are essentially remote-controlled boats just large enough to be equipped with a towfish that can be auto-deployed and recovered. Management told me recently that they see this as a potential growth opportunity as they are seeing most NATO navies order 6-10 at a time. I gather that the idea would be to form something of a fleet that could be deployed and scan a large area in a short amount of time by working together. Also, if one were to get hit by a mine, there would be no loss of life and the dollar cost would be far less than even small manned naval vessels.

XLUUVs are another emerging market. They are outside the scope of Kraken, but I see them as a big opportunity because many of the teams and companies building these are focusing on the tech required to fulfill complex missions (disable mines, destroy submarines, etc) and are made to be outfitted with a variety of third-party sensors and batteries. As management recently stated, they sell batteries and sensors as the “ears and engines” of these XLUUVs and make around $10MM per unit. Outfitting only a few units per year would move the needle for Kraken in a big way.

Finally, the RaaS business is mostly non-defense and they operate in many large and growing markets. By my estimates, they announced ~$24MM in RaaS contracts last year, up from ~$6MM the year before. I think the TAM here is very large and they have a lot of runway as their potential customers include giant industries like oil & gas, offshore wind, subsea mining, and subsea cables.

When I put it all together, I see a clear path to $200-300MM in annual revenue based on current products and the current operating environment. And if unmanned surface vessels, XLUUVs, and other adjacent markets take off, I could argue a path to $500MM in annual revenue.

For what it’s worth, in the company’s current presentation they quote their addressable market as “the global maritime robotics and services market estimated at $30 billion.” I personally don’t put much stock into this TAM estimation, especially since I’ve asked them to break this number down and they sidestepped the specifics, but I think it’s useful to demonstrate that while Kraken is a best-in-class player in several niche markets, there are still many more markets to be explored within their wheelhouse.

So while the business won’t scale into a multi-billion dollar enterprise in its current form, I think there is plenty of opportunity left. Also, one of the things I’ve found most impressive while studying Kraken has been their ability to add products to their offering, often through acquisitions. The company started off just selling SAS sensors and have acquired the battery and most of the RaaS business. I think that they’ve proven themselves savvy enough expanding the company that it’s worth assigning reasonable odds to their ability to continue expanding their products. One of Greg’s recent slides showed Kraken’s progression from sensors to components to towfish to RaaS. At the end of the timeline going into the future, he mentioned subscription-based data analytics/software, which could be an interesting new field for them to enter and would help with the lumpiness of their contract-dependent revenue.

Contract Pipeline

Kraken announces all (or nearly all) of its revenue-generating contracts via press releases, which makes it possible to reconcile where revenue is coming from. The language in many of the press releases also gives us visibility into when cash flows will occur, as sometimes contracts are one-off deals and other times they last many years.

I’ve gone through all of Kraken’s press releases and estimated cash flows for each year and product line using my best judgment. You can view the full data table here. I’ve also added Kraken’s revenue guidance they give early each year and their reported revenue for past years. While revenue and cash flow won’t perfectly line up, this should give us two things:

- We can compare past estimated cash flow based on press releases with reported revenue to see how good of a proxy it is.

- We can look into the future and estimate how much future revenue is already accounted for with signed contracts.

I believe #2 above is especially important because one of the factors that I believe has held Kraken back is their lumpy revenue driven by short-term contracts rather than recurring revenue. This creates the illusion that Kraken is riskier to invest in because if they land a large contract in one year (like the Danish, Polish, or Canadian contracts), then fail to attract new business the next year, they could see a significant decline in revenue.

While this is a valid concern and in a perfect world the business would lock customers in with indefinite recurring revenue, I believe that all of the $72MM guided revenue for 2023 is already accounted for and at least $28MM of 2024 revenue has also been booked.

Furthermore, my estimated cash flows for 2021 and 2022 combined exceed reported revenue over that time period by $27MM. I believe the reason for this gap is that I’m not spreading out the cash flows over enough years to accurately reflect the terms of the contracts, especially the large contracts with the Polish, Danish, and Canadian Navies. For example, I know the Polish contract was for three Katfish and in an email in mid-May I was told they’ve delivered one so far. It’s likely they’ve only been paid for one unit so far and that the other two will be paid for when they’re delivered.

I’m working with Kraken’s investor relations to confirm this theory and create a more accurate cash flow projection based on their press releases, but for the time being, it is possible that in addition to the $72MM of cash flow booked for 2023 and $28MM booked for 2024, there is also an extra $27MM of booked cash flow from 2020-2022 that needs to be spread out over the next couple of years.

Putting all of this together, on the low-end Kraken has combined $100MM of booked cash flow for 2023 and 2024 that is virtually guaranteed to be realized, and that value could be as much as $127MM. Given that the company trades at $117MM market cap, I believe the market hasn’t fully priced in the value of these contracts and that the stock price could rerate as revenue numbers are officially reported.

And just to add a little extra sauce on top, their service-based RaaS business segment did $24.5MM in announced cash flow last year and so far they’ve only announced $1.5MM in 2023. It’s possible that this line of business isn’t doing as well this year, but last year rather than announce every project as it happened, they waited until later in the year and announced the completion of several projects in each press release. If you consider this and the fact that they announced revenue guidance before their $16MM battery sale, I think it’s likely that 2023 revenue exceeds their mid-point guidance of $72MM, perhaps significantly.

And keep in mind that we aren’t even halfway through 2023 and haven’t started 2024, so there is likely to be more contracts and revenue announced in the next 1.5 years given how the company has grown consistently over the last five years.

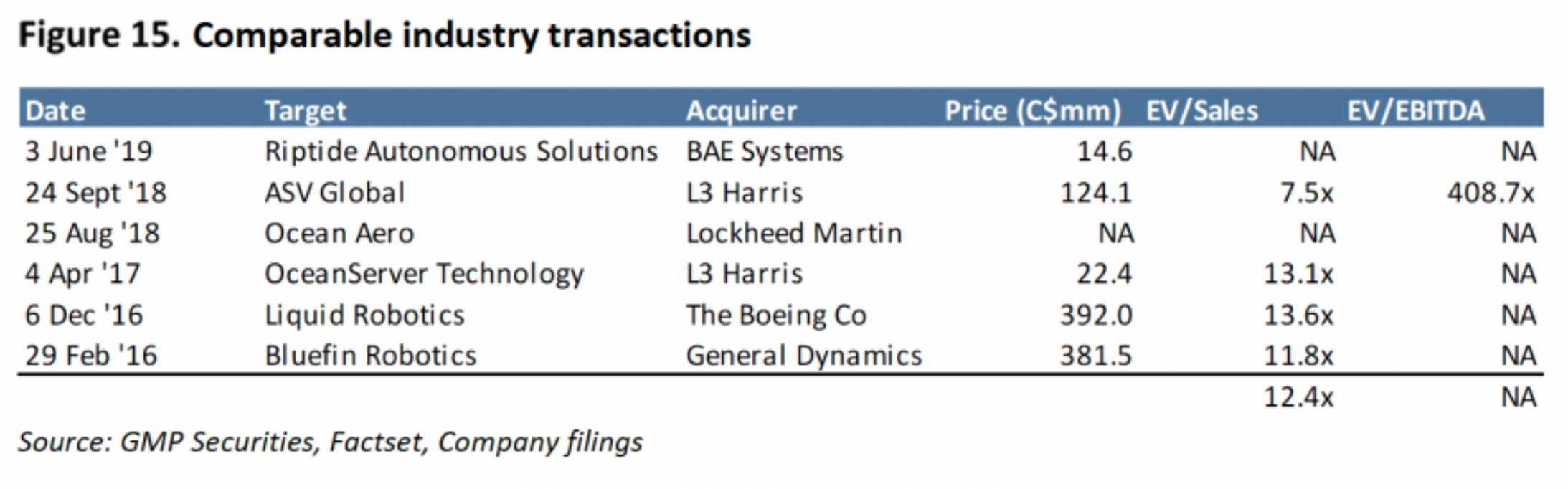

Valuation

Finding apples-to-apples valuation comps is difficult because most of Kraken’s competitors are large defense contractors who have a small subdivision that works on similar technology. Here is a table of similar acquisitions to Kraken that I came across:

This list was compiled before COVID and doesn’t take into account more recent acquisitions. Anduril did not disclose how much they purchased Dive Technologies for, but given that Dive’s units use Kraken sensors, software, and batteries, I don’t think it’s a stretch to assume Anduril would be an interested party, especially given the fact that they just raised $1.5 billion USD in December 2022.

I believe Kraken will transition into a profitable company sometime in the next 1-2 years. On a trailing basis, their previous four quarters produced positive free cash flow for the first time. Earnings are still slightly negative, but I expect larger Katfish and battery orders to meaningfully contribute to an inflection in earnings. A few years ago, the company was bidding for $500k sonar contracts; now they are bidding for $10MM battery contracts and $50MM Katfish projects. They’ve developed several great products, and now that they’ve built a reputation, it’s more a matter of selling, which should carry less relative expense and risk.

Kraken has a current EV around $125MM. If you believe my estimated cash flow calculations using their press releases, they should easily hit their $72MM mid-point 2023 revenue guidance, if not exceed it. That implies a current EV/sales of 1.74. Given that they have grown revenue >50% annualized over the last six years and are on the brink of profitability, I don’t think it’s a stretch to argue that their fair value could approach 10x EV/Sales, especially when the comps in the table above averaged 12.4x EV/sales. 10x EV/Sales would imply a $720MM EV, which maps to a $712MM market cap, >500% upside.

Looking forward towards profitability, if they are able to hit their guided 20% EBITDA margins this year and their long-term goal of 30% EBITDA margins in 2024, the company could quickly flip to producing significant FCF relative to current market cap. Even if we assume revenue growth stalls out at $72MM in 2024 and they hit 30% EBITDA margins with their recent capex rate of $5-6MM/yr, they could produce ~$15-17MM FCF in 2024.

I believe the number will actually be higher as I expect revenue to continue to grow. If they hit their revenue guidance and the business continues to grow at its long-term growth rate, they could reasonably eclipse $100MM in 2024. Using the same parameters as above, I get ~$25MM FCF.

One of the weakest aspects of this investment idea is that there isn’t much of a margin of safety, so potential losses are difficult to estimate. It’s possible that business dries up and the company begins to shrink looking forward into 2024 and 2025, though I find that argument to be weak given that they have grown steadily for so long and that the macro environment should continue to be a tailwind for Kraken. They also have a diverse set of offerings and it’s unlikely all of them would decline simultaneously.

Risks

- We make it through the mine-hunting UUV replacement cycle and the larger navy contracts dry up.

- No dilution in 2022 was a blip and the company reverts back to the old habit of issuing lots of stock.

- Management is unable to control costs and EBITDA margins remain too low to support FCF and earnings.

- Karl continues to sell large volumes of stock every time the company announces good news, putting a dampener on the share price.

- Supply chain issues impact components they need to fulfill orders.

Catalysts

I think that Kraken officially reporting 2023 financials will be a catalyst. If they hit their guided $14.5MM EBITDA with $5.5MM capex, they should be both FCF and earnings positive this year. How many profitable companies growing at 50%/yr and with expanding margins trade at <2x sales and <8x EBITDA?

While I doubt that shares will rerate in a quick jump, I think that if Kraken continues to execute, they will both continue to grow and multiples will expand over the next 2-3 years.

Another medium-term possibility is that Kraken is acquired by a larger defense contractor. Anduril is cashed up and all of the large defense contractors are likely looking for ways to expand in this important space. Would Kraken be taken out at a full 10x EV/Sales valuation like other recent acquisitions in the space? It seems like a stretch given the current share price, but it’s possible, and even a 5x takeover would yield great returns.

Disclosure

I own shares of Kraken Robotics at the time of writing and may buy or sell shares at any time without notice or warning. This write-up contains my thoughts and opinions and is not investment advice. I may have made mistakes. Do your own due diligence and review my legal disclaimer.