Whiteout Capital

Private investor publishing independent research focused on microcaps.

LiveOne (LVO)

Published: Mar 23, 2023

LiveOne (LVO): Special situation with two pending spinoffs that are each expected to trade higher than the market cap of the company.

Summary

LiveOne is a media and audio company with four main segments:

- Slacker Radio: membership music streaming service (pre-installed on every Tesla sold, with Tesla paying the monthly fee indefinitely)

- PodcastOne: podcast company monetized with ads

- PPVOne: live stream PPV events to concerts, music festivals, artist signings, etc.

- CPS: customized clothing, jewelry, and other merchandise for artists

While I think there is an argument to be made for the long-term potential of the company in each of these business segments, my primary focus for this write-up is an event-driven situation that should play out by the end of 2023.

2023 event-driven thesis

LVO’s PodcastOne owns a collection of 155 podcasts with 2.3 billion annual downloads and currently accounts for ~35% of revenue. LVO recently announced that they plan to spinoff PodcastOne in the first half of 2023, which would create the only publicly-tradable pure play podcast stock. The company plans to retain ownership and return funds raised through the IPO via a special dividend of 5-10% to common equity holders.

In mid-February, LVO announced that a third party (ValueScope) valued the company at $230-274m as of late December 2022. For context, LVO currently trades at ~$110m EV. The record date for the transaction is set for April 7th, though there have been several delays as they are working with regulators to approve the spinoff and special dividend.

For the sake of coming up with a starting valuation, let’s say LVO issues a 10% special dividend and IPOs PodcastOne at a $230m valuation (the low end of the third-party valuation).

If we assume PodcastOne’s EV is proportional to its share of LVO’s revenue, that implies a $110m*0.65=$71.5m EV for the rest of the company. Now back in 90% post-IPO ownership of PodcastOne at a $230m valuation, and we’re in the ballpark of $278.5m EV for LVO, or 153% upside, plus a 10% special dividend.

LVO has stated that they won’t spin off PodcastOne for less than $150m. Using the same math above, this implies an EV of $110m0.65+$1500.9=$206m, or 88% upside, plus a 10% special dividend.

The downside case is that the spinoff is canceled, in which case I expect the stock to stay flat, all else being equal. There isn’t a great margin of safety since the company is not profitable, but later on in the “Margin expansion” section, I make the argument that even without the spinoff, LVO is cheap at these levels.

Furthermore, LVO plans to also spinoff Slacker (the largest segment of the business) later in 2023, which would also likely be beneficial for shareholders, though specifics on valuation and timing have not yet been announced.

Why does this price dislocation exist? I believe it’s a combination of a covid windfall obscuring financials and high customer concentration in Slacker…

Covid windfall obscuring financials

The stock has been decimated over the last two years. LVO saw a huge covid boost as products such as their concert PPV streams exploded in popularity, but the downfall as we’ve returned to normal has been disproportionately brutal. The share price briefly reached highs above $5 in 2021 and now trades around $1 after hitting lows around $0.48 in the autumn of 2022.

2022 revenue declined 15%, which I believe is the main reason why the stock has been punished, though I’d also argue this revenue decline is the result of a one-time covid windfall inflating 2021 results and masking more steady growth in PodcastOne and Slacker, the core segments of the business.

Note, I’m using nine months ended Dec 31 financials from LVO’s 10-Q’s in February of each year to compare rather than full-year numbers since they have not yet released their 2022 annual report and I’d like to make apples-to-apples comparisons.

The “Membership services” line is mostly Slacker revenue and the growth there can be attributed to Tesla’s growth in car volume. From their most recent 10-Q, the “Advertising” line is “primarily attributed to our growth in PodcastOne over the period.” They state more specifically elsewhere that PodcastOne accounts for 35% of revenue, and if we take the 2022 revenue values from above, the “Advertising” line equals ~35% of total revenue, so I think “Advertising” is a solid proxy for what the financial statements of PodcastOne on its own would report.

While LVO’s topline revenue declined 15% LTM, which looks bad at face value and makes the company screen poorly, their two core assets (Slacker and PodcastOne) both grew in 2022.

I believe that most of the share price decline is the result of a “covid hump” working its way through the financials, making it look like the company is shrinking when the core lines of revenue are actually expanding.

Let’s dig in…

The company hosted Social Gloves in 2021, which was a one-time event that brought in a lot of revenue counted under “Sponsorship and licensing” and “Ticket/Event,” as well as Spring Awakening Music Festival, which contributed to “Ticket/Event.”

“Merchandise” is its own separate line of business and had some covid bump, but I’ll ignore that in this analysis.

If you look at the images above, you can see the covid hump creating a one-time windfall in these two segments in 2021, with nine month ended Dec 31 revenue for “Sponsorship and licensing” and “Ticket/Event” going from $301m (2019) → $4,972m (2020) → $25,582m (2021) → $1,192m (2022). 2020 likely saw a less pronounced bump from more general interest in virtual concerts, and 2021 had a huge windfall related to Spring Awakening Music Festival and Social Gloves.

If we estimate the live event business would have done revenue in 2020 and 2021 equal to 2022 if covid hadn’t happened, we get a total covid windfall of $4,972m-$1,192m + $25,582m-$1,192m = $28,170m.

If you look only at “Subscription services” (aka Slacker) and “Advertising” (aka PodcastOne), nine months ended Dec 31 revenue increased $28,479m (2019) → $38,401m (2020) → $54,946m (2021) → $64,364m (2022).

“Advertising” (aka PodcastOne) alone in the same period did $1,814 (2019) → $13,453 (2020, year LVO acquired PodcastOne for $16m) → $25,286 (2021) → $26,138 (2022). The 3% growth in 2022 isn’t great, but it’s a lot better than the -15% the company reported. 2022 wasn’t a good year for advertisers in general, and while this low growth rate is somewhat lackluster, it’s still better than the -1% META did in 2022.

To summarize, LVO has done $95m LTM revenue, with its core lines of business growing each of the last three years. As a result of covid, they were a beneficiary of a ~$28m one-time windfall in 2021, which was a huge positive for the company. However, this windfall is now making the company look like its shrinking, and investors have responded by placing the stock in the penalty box.

If the covid windfall never happened and topline revenue showed progressive growth, would the stock trade at just over 1x sales? I’d bet not. I think that when PodcastOne is spun out and investors see its separate financials, they will value the company at much higher multiples, which is likely how ValueScope arrived at their valuation.

Share repurchases

LVO bought back ~$2m worth of stock last year and has authorized another $2m buyback this year. While the company has diluted in the past to fund acquisitions (at ~10%/yr), I don’t see much risk of dilution in the near term and expect share count will either flatline or decrease slightly.

In a way, I see these repurchases as being partially possible because of the covid windfall. They’ve essentially been able to push some of the ~$28m windfall into buybacks as the share price has been slammed.

Slacker and Tesla

LVO has a partnership with Tesla and a subscription of Slacker Radio is included in all new vehicles sold, with Tesla footing the monthly bill indefinitely.

If you’re a Tesla fan, that makes LVO a way to bet on Tesla’s growth without paying for the high valuation of Tesla’s common shares.

Each Tesla unit sold increases LVO’s subscription revenue, so it doesn’t matter if Tesla’s margins shrink, LVO gets paid per unit, and Elon has made it clear with the string of recent price cuts that his goal is to sell a lot of affordable EVs, even at the expense of profits. In many ways, I think Slacker is a better business model.

There is of course the risk that Tesla terminates their partnership with Slacker, but there is no indication that a breakup is impending, and there never has been. I believe this large concentration of revenue in Tesla is a big reason why the company trades so cheap.

However, I think investors’ worry about the concentration is overblown. Tesla accounted for ~43% of LVO’s revenue LTM, or about $95m*0.43=$41m Slacker revenue. Tesla is a $500b EV company projected to do $106b in revenue next year. The Slacker cost is a rounding error to them and I’d be surprised to see them cut the cost, especially since the free subscription enhances the “affordable-luxury” branding of their cars.

Furthermore, they sold 1,313,581 cars in 2022. Tesla is paying for Slacker subscriptions long-term in all of their sold units, but even if you assume the $41m cost last year came only from their new units sold, that implies a per-unit cost of $41m/1,313,581=~$31. The actual incremental cost to Tesla for each new unit sold is likely several times lower.

The risk of Tesla terminating the partnership is a real risk, and the stock would surely suffer if that ever happened, but I think the partnership is mutually beneficial. Including a free Slacker subscription is a cheap and differentiating feature for Teslas with the overall cost being nearly negligible to the overall company. Yet LVO is small enough that this revenue stream should help the company sustain strong growth for years to come.

Should Slacker also be spun out in 2023, I believe it could also trade at a higher multiple than LVO.

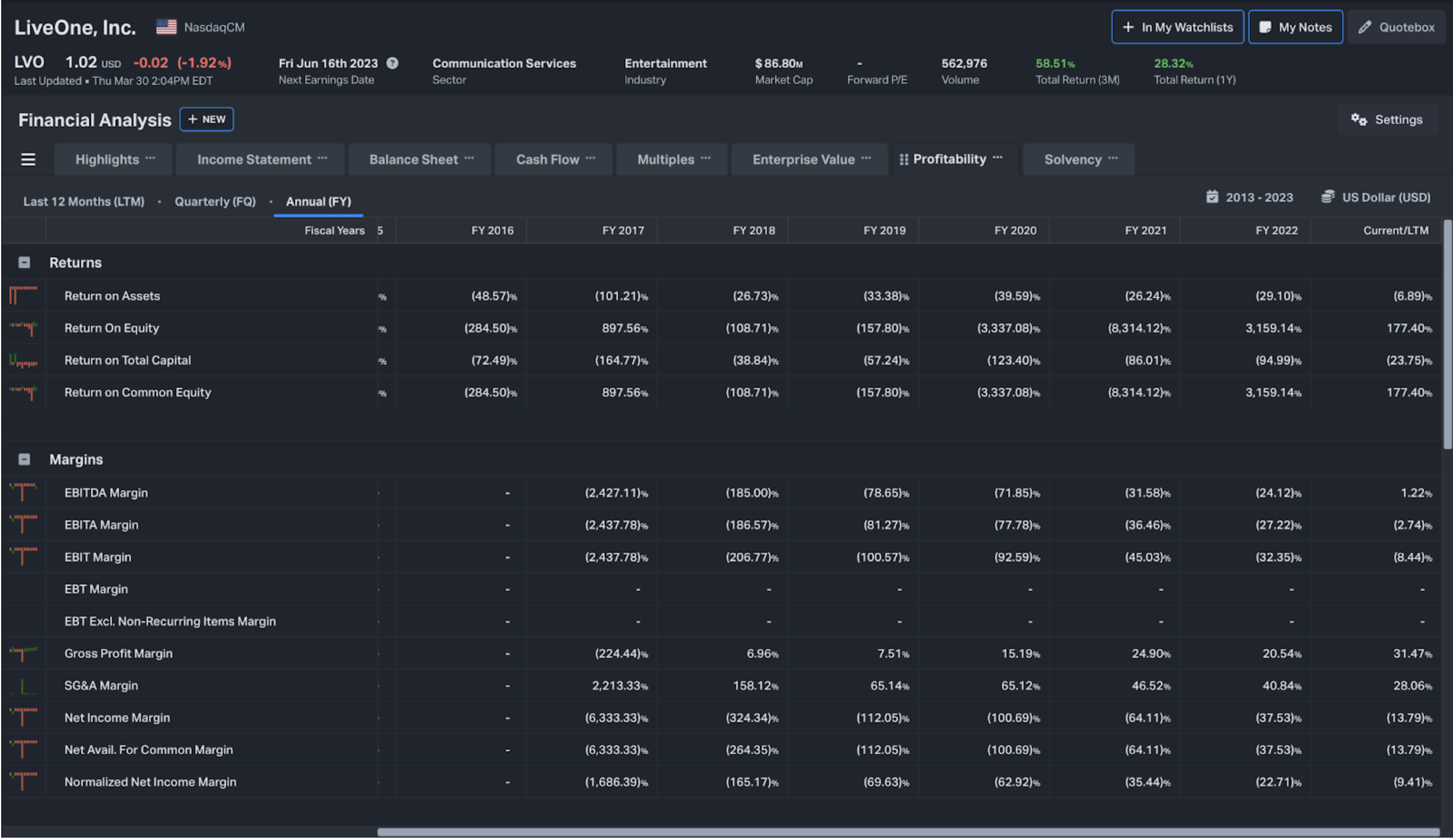

Margin expansion

Most of my thesis is focused on the imminent spinoff of PodcastOne and the near-term spinoff of Slacker, but I also think LVO could be a longer-term investment. Margins have expanded each of the last five years, which is illustrated in the image below. Gross margin, EBITDA margin, EBIT margin, and net income margin have all sequentially and steadily improved, moving the company closer to profitability.

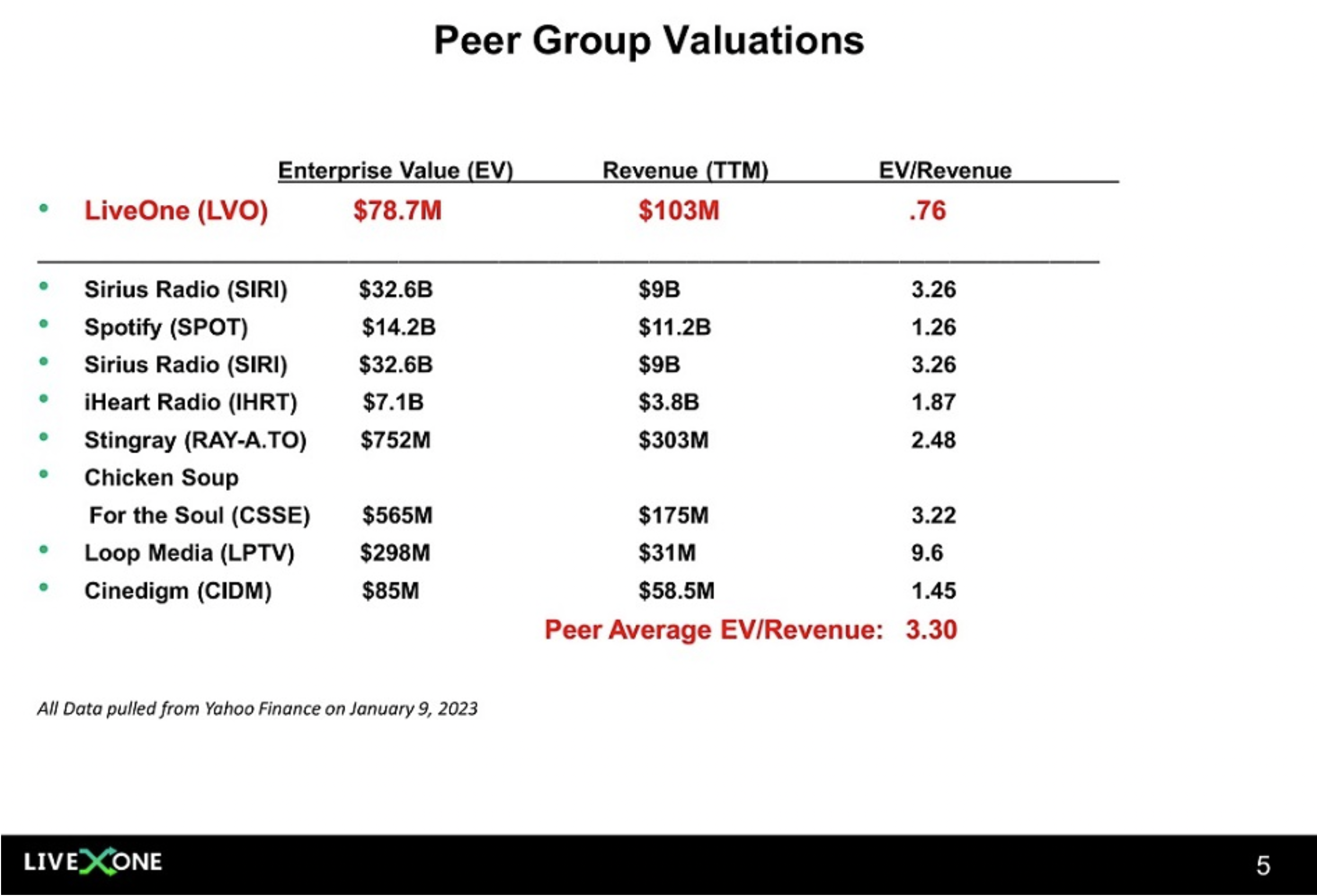

The company trades at ~1x EV/sales, which not only seems low for a company that I believe can sustain 20% growth and will continue to expand margins, but is also low relative to peers. Here is a peer group comparison from LVO’s most recent slide deck (note that the values today would be slightly different, but there is still a large disconnect).

Despite the company growing revenue from $7m in 2018 to ~$100m this fiscal year (including the 15% decline) while expanding margins, share price is down 75% over that timeline and has recently traded at or near all-time lows.

Track record of Robert Ellin, CEO

Robert Ellin is the CEO and owns ~22% of the company, with total insider ownership of ~24%. There are frequent insider purchases by Ellin and others going back several years.

One could argue that the size of the transactions relative to the net worth of the individuals and their overall ownership in LVO is small, but what I find more important is that there is not a single insider sale in the last four years (ignore the two ~$100 transactions in 2020)—everyone involved is committed and I think clearly believes there is still immense value potential despite the share price decline.

Robert Ellin is not the founder of the company but is an LA-based hedge fund manager with a proven track record over several decades of investing in and operating small and micro-cap companies. Most notably, Ellin founded Mandalay Digital which became Digital Turbine (APPS), which grew from a company with $4m revenue in 2013 to LTM revenue of $710m and net income of $51m.

The share price of APPS also declined significantly in 2022, but is still up considerably over the long term. Ellin has previously stated that he sees even more potential for LVO than he did for APPS.

I believe that Ellin has executed a sound strategic M&A playbook at LVO and is now ready to unwind things by spinning them out and creating shareholder value. To the best of my judgement, he is not an empire builder and his incentives and goals are strongly aligned with shareholders.

Risks/criticisms

- The Slacker Radio segment is heavily concentrated in Tesla, who pays for a subscription in nearly all of their vehicles. A main risk and criticism of the last several years is that being so concentrated opens up significant downside risk. This is a valid concern, though they have been in a steady relationship with Tesla for many years and there is currently no indication that Tesla plans to switch providers, cut costs, etc. given that the cost to Tesla is low and Slacker adds to their branding. The customer concentration is uncomfortable, but I think the perceived risk is generally overblown and concentration has been steadily decreasing as other segments of LVO continue to grow.

- The company has been assembled mostly through dilutive acquisitions rather than organically, and that trend is unlikely to change as the company is not profitable. I think there are arguments to be made that LVO is 2-3 years out from being able to fund future acquisitions with debt and FCF, but that is mostly speculation. Regardless, I believe the market underappreciates the organic growth potential within their current portfolio of assets.

- There is not a substantial margin of safety, as the company is still unprofitable, and while I do believe the share price is cheap, it could easily go from 1x EV/sales to 0.5x EV/sales when there are no profits to fall back on.

Catalysts

- Spinoff of PodcastOne in the first half of 2023

- Spinoff of Slacker in the second half of 2023

- Rerating of LVO as the “covid hump” works its way through the financials and the company starts showing topline growth again, likely in 2023 as YoY financials flip back to growth.

- The company reaching profitability, perhaps in 2024.

Disclosure

I own shares of LiveOne at the time of writing and may buy or sell shares at any time without notice or warning. This write-up contains my thoughts and opinions and is not investment advice. I may have made mistakes. Do your own due diligence and review my legal disclaimer.